North America Aircraft Landing Gear Market Overview - Definition, scope, and significance?

The North America Aircraft Landing Gear Market comprises the design, manufacture, and support of landing‑gear systems for fixed‑wing airplanes, helicopters, and military aircraft operating within the United States, Canada, and Mexico. It includes main and nose gear, various gear arrangements (tricycle, tandem, tail‑wheel), and serves commercial airlines as well as armed forces. The market is a critical component of aerospace safety and performance, influencing aircraft weight, fuel efficiency, and runway compatibility, thereby underpinning the region’s robust aviation sector.

North America Aircraft Landing Gear Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include a growing commercial fleet, renewal programs for military aircraft, and increasing demand for lightweight, high‑strength gear assemblies. Technological advances such as composite materials and predictive maintenance create opportunities for higher efficiency and aftermarket services. Restraints stem from high capital requirements, stringent certification processes, and supply‑chain volatility for raw alloys. Challenges involve fluctuating fuel prices that pressure airlines to seek lighter gear solutions, while opportunities arise from the emergence of electric‑propulsion aircraft requiring novel landing‑gear designs.

North America Aircraft Landing Gear Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward integrated landing‑gear systems that combine shock absorption, steering, and braking functions into compact modules. Manufacturers are investing in digital twins and simulation tools to shorten development cycles. Emerging trends include the adoption of additive manufacturing for complex gear parts and the integration of health‑monitoring sensors that feed real‑time data to maintenance platforms, enhancing reliability and reducing downtime.

COVID-19 Impact on the North America Aircraft Landing Gear Market - Pandemic effects and recovery trajectory?

COVID‑19 caused a temporary slowdown in new aircraft orders and delayed maintenance schedules, reducing short‑term demand for new landing‑gear units. However, the market demonstrated resilience as airlines accelerated fleet‑retirement programs and airlines shifted focus to newer, more fuel‑efficient aircraft, reigniting demand for advanced gear solutions. Recovery is now underway, supported by robust defense spending and a rebound in commercial travel, positioning the market for a steady upward trajectory.

North America Aircraft Landing Gear Market Competitive Landscape - Major competitors and market consolidation?

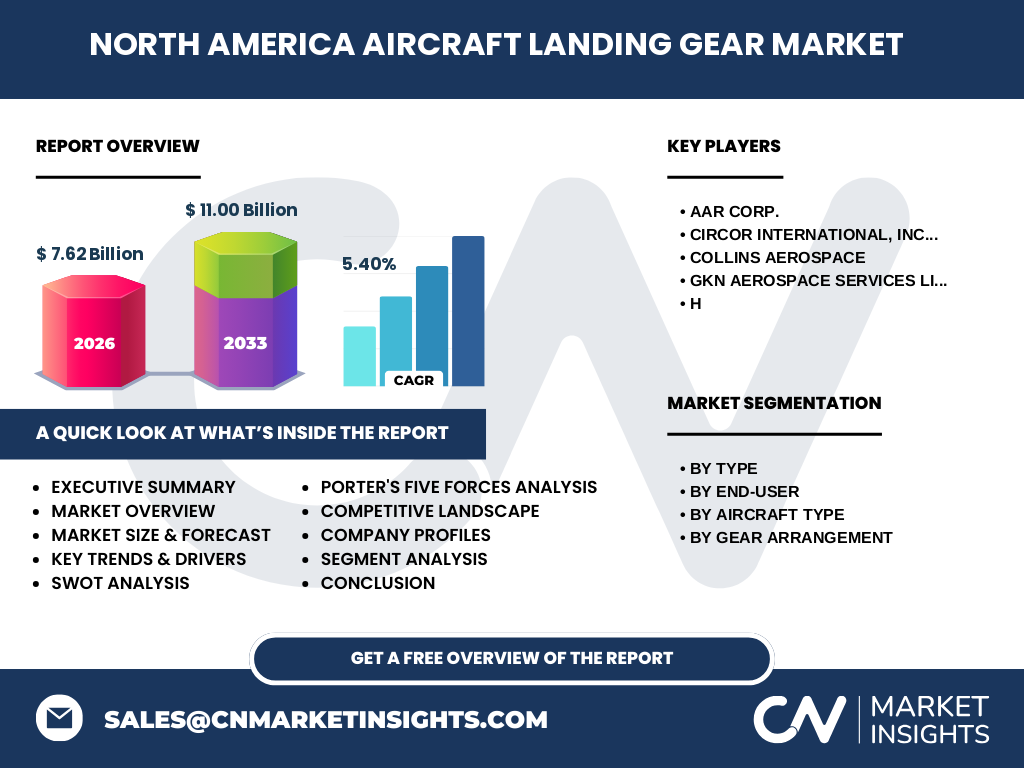

The competitive environment features a mix of established aerospace giants and specialized suppliers. Key players such as AAR Corp., Collins Aerospace, GKN Aerospace Services Limited, Circor International, Inc., and others dominate the market through extensive product portfolios and global service networks. Recent years have seen strategic acquisitions and joint ventures aimed at expanding capabilities in lightweight materials and digital services, reinforcing consolidation trends while preserving niche expertise.

Executive Summary - High-level overview and key findings about North America Aircraft Landing Gear Market?

The North America Aircraft Landing Gear Market is valued at USD 7.62 billion in 2026 and is projected to reach USD 11.00 billion by 2033, reflecting a CAGR of 5.40 %. Growth is fueled by commercial fleet expansion, military modernization, and technology‑driven product innovation. While capital intensity and regulatory compliance pose challenges, opportunities abound in lightweight composites, sensor‑enabled health monitoring, and additive manufacturing. Competitive dynamics are shaped by leading OEMs and strategic collaborations.

North America Aircraft Landing Gear Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 5.40 %, the market is expected to maintain a steady upward trajectory from 2025 through 2032. The forecast indicates incremental growth each year, driven by continued aircraft deliveries, replacement cycles for aging gear, and increasing demand for advanced, maintenance‑friendly systems. This sustained expansion underscores a robust investment environment for manufacturers and service providers.

North America Aircraft Landing Gear Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type divides the market into main gear and nose gear, each serving distinct load‑bearing functions. End‑user segmentation separates commercial aviation from armed forces, with commercial airlines accounting for the larger share due to higher fleet numbers. Aircraft type segmentation distinguishes airplanes from helicopters, where airplanes dominate but helicopters present niche growth. Gear‑arrangement segmentation includes tricycle (most common in commercial jets), tandem, and tail‑wheel configurations, each catering to specific aircraft designs.

Global North America Aircraft Landing Gear Market Size and Share by Region - Geographic distribution?

Within the global context, North America holds a leading position, contributing the majority of the market’s USD 7.62 billion valuation in 2026. The region’s advanced aerospace infrastructure, high aircraft utilization rates, and substantial defense budgets drive its outsized share relative to other continents. While exact percentages are not disclosed, North America remains the primary hub for landing‑gear innovation and production.

Regional Analysis of the North America Aircraft Landing Gear Market - Detailed regional market performance?

The United States dominates regional performance, home to the largest commercial airlines, major defense contracts, and leading OEMs. Canada contributes through a strong general aviation sector and defense procurement, while Mexico shows emerging growth driven by increasing regional airline activity. Each sub‑region benefits from local supply chains, skilled labor pools, and supportive regulatory frameworks that enhance market stability.

Leading Company Profiles in the North America Aircraft Landing Gear Market - Industry players and strategies?

AAR Corp. focuses on aftermarket support and retrofit solutions, leveraging a global service network. Collins Aerospace emphasizes integrated systems and digital services, investing heavily in sensor technologies. GKN Aerospace Services Limited offers high‑performance gear components using advanced composites. Circor International, Inc. specializes in hydraulic and pneumatic subsystems that complement landing‑gear functionality. These firms pursue strategies such as R&D investment, strategic partnerships, and portfolio diversification to maintain competitive advantage.

Porter's Five Forces Analysis of the North America Aircraft Landing Gear Market - Competitive forces assessment?

• Threat of new entrants: Low, due to high capital requirements and regulatory barriers. • Bargaining power of suppliers: Moderate, as specialized alloys and composite materials are limited in number. • Bargaining power of buyers: High for major airlines and defense agencies, which demand cost‑effective, reliable solutions. • Threat of substitutes: Low, because landing gear is a non‑replaceable safety component. • Competitive rivalry: Intense, driven by technological innovation and service differentiation among established players.

SWOT Analysis of the North America Aircraft Landing Gear Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established OEM base, strong R&D capabilities, robust defense spending. Weaknesses: High production costs, dependency on a few key raw‑material suppliers. Opportunities: Adoption of lightweight composites, growth of electric‑propulsion aircraft, expansion of predictive‑maintenance services. Threats: Economic cycles affecting airline capital expenditures, potential trade restrictions on critical materials, rapid technology turnover imposing upgrade pressures.

North America Aircraft Landing Gear Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material sourcing (high‑strength alloys, composites), followed by design and engineering, component manufacturing, assembly, and testing. Aftermarket services—including inspection, repair, overhaul, and parts supply—represent a significant revenue stream. Digital platforms for health monitoring link OEMs with operators, creating a feedback loop that fuels continuous improvement and aftermarket demand.

Key Investment Insights in the North America Aircraft Landing Gear Market - Strategic investment recommendations?

Investors should focus on companies advancing composite‑based gear technologies and those building robust aftermarket service networks. Partnerships that enhance digital health‑monitoring capabilities are likely to yield high returns. Allocation toward firms with diversified end‑user exposure (commercial and military) can mitigate cyclical risk, while targeting firms engaged in strategic acquisitions may capture faster market share growth.

North America Aircraft Landing Gear Market Conclusion - Summary and key takeaways?

The market’s solid base of USD 7.62 billion in 2026 and projected growth to USD 11.00 billion by 2033 underscore a healthy, expanding sector. Core growth drivers include fleet modernization, advanced material adoption, and digital maintenance solutions. While high entry barriers and supply‑chain dependencies persist, the combination of strong commercial demand and sustained defense investment positions the North America Aircraft Landing Gear Market as an attractive arena for long‑term strategic investments.

Research Methodology - How this research was conducted?

Data were collected from primary interviews with industry executives, supplier surveys, and secondary sources such as company filings, aerospace trade publications, and government procurement records. Quantitative analysis applied the provided market size and CAGR to generate forecast figures. Qualitative insights were derived from trend observation, competitive positioning, and expert commentary, ensuring a comprehensive view of the market landscape.

Research Scope - Coverage and limitations?

The study covers North America, focusing on landing‑gear systems for commercial and military aircraft across all major gear types and arrangements. It includes market size, segmentation, competitive analysis, and forecasts to 2033. Limitations stem from the reliance on publicly available data; proprietary supplier cost structures and confidential defense contract values were not disclosed, and thus are not quantified in the report.

Key Companies and Recent Developments in the North America Aircraft Landing Gear Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

AAR Corp. announced a new retrofit program for legacy cargo aircraft, enhancing payload capacity with lightweight gear components. Collins Aerospace unveiled a sensor‑integrated landing‑gear platform that streams real‑time load data to airline maintenance systems. GKN Aerospace Services Limited introduced a carbon‑fiber main‑gear bracket, reducing weight by 15 % compared with traditional alloys. Circor International, Inc. entered a joint venture with a hydraulic‑system specialist to develop next‑generation actuation units for tandem‑gear aircraft. These developments reflect the market’s focus on weight reduction, digitalization, and collaborative innovation.